Search here

Search here Log In

Log InMutual Funds Industry In Pakistan

The financial year 2014-2015 remained challenging for the Mutual Funds Industry. The assets under management slightly increased from PKR 416 billion on June 30, 2014 to PKR 443 billion as on June 30, 2015. The assets under management stood at PKR 458.37 billion on December 31, 2014. The Government again changed the tax policies creating unease amongst the investors. The economic growth remained broad based. According to provisional estimates the GDP growth during 2014-15 remained at 4.24% as compared to last year's revised estimates of 4.03%. The total investment to GDP during FY 2014-15 improved at 15.1% (Provisional Estimate) as compared to last year revised 14.9% during current fiscal year. Savings improved to 14.5% of the GDP as compared to revised rate of savings to GDP of 13.7%. Despite this modest improvement, rigorous steps are required to promote savings and investments with major focus on investors’ awareness and education as well as removing the taxation anomalies and regulatory issues hampering the growth. The Government should encourage long term investments and take measures to incentivize the long term savings.

Background:

Internationally, mutual funds have been around for a long time, dating back to the early 19th century. The first modern American mutual fund opened in 1924, yet it was only in the 1990's that mutual funds became mainstream investments, as the number of households owning them nearly tripled during that decade, with recent surveys showing that over 88% of all investors in the US participate in mutual funds.

Pakistan was in the forefront amongst developing countries in initiating Mutual Funds. The first open-end mutual fund was introduced in 1962 and closed-end mutual funds from 1966. These were state owned. In 1971, the rules were introduced to allow private sector companies to launch closed-end mutual funds. The first private sector closed-end fund was launched in 1983. Mutual Funds Association of Pakistan (MUFAP) was formed in 1996 when a group of investment advisors managing eight closed-end mutual funds got together to form an association that would work to promote mutual funds in Pakistan. Around the same time, the Asset Management Companies Rules, 1995 had been notified which allowed private and foreign firms to launch open-end mutual funds. While the first one open-end mutual fund was launched in 1997, it wasn’t before 2002 that this area started to really pick up pace when several other players entered the industry. The same period also saw the stock market’s performance scale new heights as a result of positive government policies and incentives, registering a growth of more than fifteen times in the net assets of the mutual funds between the years 2003-2008. The financial crisis of 2008 curbed the growth pattern as the economy and the financial markets drastically declined and subsequently the mutual funds declined. A number of ad-hoc measures taken by the regulator and the stock exchanges with the approval of the regulator, further fuelled the downfall and industry went through a rough period. Post 2008, the industry has been slowly and gradually trying to recover and regain its growth momentum. However lack of understanding as to the dynamics and importance of the mutual fund industry in the economy led to tax policies by the Government which has severely affected the growth of the industry. The steps taken in past few years have been detrimental for the mutual fund industry. It had been very unfortunate that the mutual fund industry has been plagued by various taxation anomalies and issues that have been growing every year rather than reaching any resolution. It is also unfortunate that the petitions filed in the Honourable Courts have been pending for years now with no outcome. These are adding to the cost of management and affecting the return of the investor.

The Government instead of facilitating savings and investments in the country has been hampering the same through taxation and other anomalies. Despite these trying circumstances the industry has been resilient in its survival and trying to bring in new innovative products that meet the investors' requirements. The fact however remains that mutual funds industry would have been much higher if it had not faced the tax anomalies that it has over the years and resources that were directed towards litigation could have been utilised to promotion and investor education so that the public at large would have been aware of what mutual funds are and mutual funds would have been a household name and first choice savings vehicle.

What Are Mutual Funds?

A mutual fund is a special type of investment vehicle that pools together money from many investors and invests it on behalf of the group, in accordance with a stated set of objectives and is managed by a professional investment company. This large pool of money gives each investor much greater purchasing power than they could possibly have investing on their own. After paying operating costs, the earnings (dividends, capital gains or losses) of the mutual fund are distributed to the investors, in proportion to the amount of money invested. Heeding the adage "Don't put all your eggs in one basket" the holders of mutual-fund shares are able collectively to gain the advantage by diversifying their investments, which might be beyond their financial means individually.

A mutual fund may be either an open-end or a closed-end fund. An open-end mutual fund does not have a set number of shares; and continuously issues and redeems units. Investors are able to buy and sell their units at any time at the prevailing Net Asset Value of the Fund depending upon the performance of the securities held by the fund. On the other hand, closed-end mutual fund has a fixed number of shares and is then traded on the secondary market, where the value of the shares fluctuates with the market.

Mutual Funds vs. Direct Investments:

Mutual funds are popular because they make investing in financial markets easy. From an investors' viewpoint mutual funds have several advantages such as:

- Professional management and research to select quality securities

- Spreading risk over a larger number of stocks whereas the investor is limited to buy only a hand full of stocks. The investor is therefore not putting all his eggs in one basket.

- Ability to add funds at set amounts and smaller quantities such as PKR 1,000/5,000 per month

- Ability to take advantage of the stock market which has generally outperformed other investments in the long run.

- Ability to convert the Units into cash at any time and receive the amount within 6 working days.

Economies of scale: Because a mutual fund buys and sells large amounts of securities at a time, its transaction costs are lower than what an individual would pay for securities transactions.

Types of Mutual Funds in Pakistan

The mutual funds industry has introduced many attractive products in the last twelve years or so which are especially attractive for the small investors/ savers and it is precisely this sector which is most important for mutual funds to target and develop. Until the end of the 1990s the only categories of mutual funds in Pakistan were equity and balanced funds in both classes of mutual funds i.e. closed end and open end. Since then, the mutual fund industry introduced many new products suited to meeting the investment needs and risk appetite of a very broad cross section of the investing public such as Pension funds, Money Market Funds, Fund of Funds, Income Funds, Capital Protected/Preservation Funds, Index Tracker Funds, Commodities Funds and Income Funds for investment return to be paid monthly, quarterly or annually. In addition, the mutual funds industry also offers Shariah compliant funds under each of the categories mentioned above. These categories of funds cater to the needs of all type of investors, those who want to invest to supplement their current income and do not want to take risk and those who want to invest for long term growth and to meet their retirement needs.

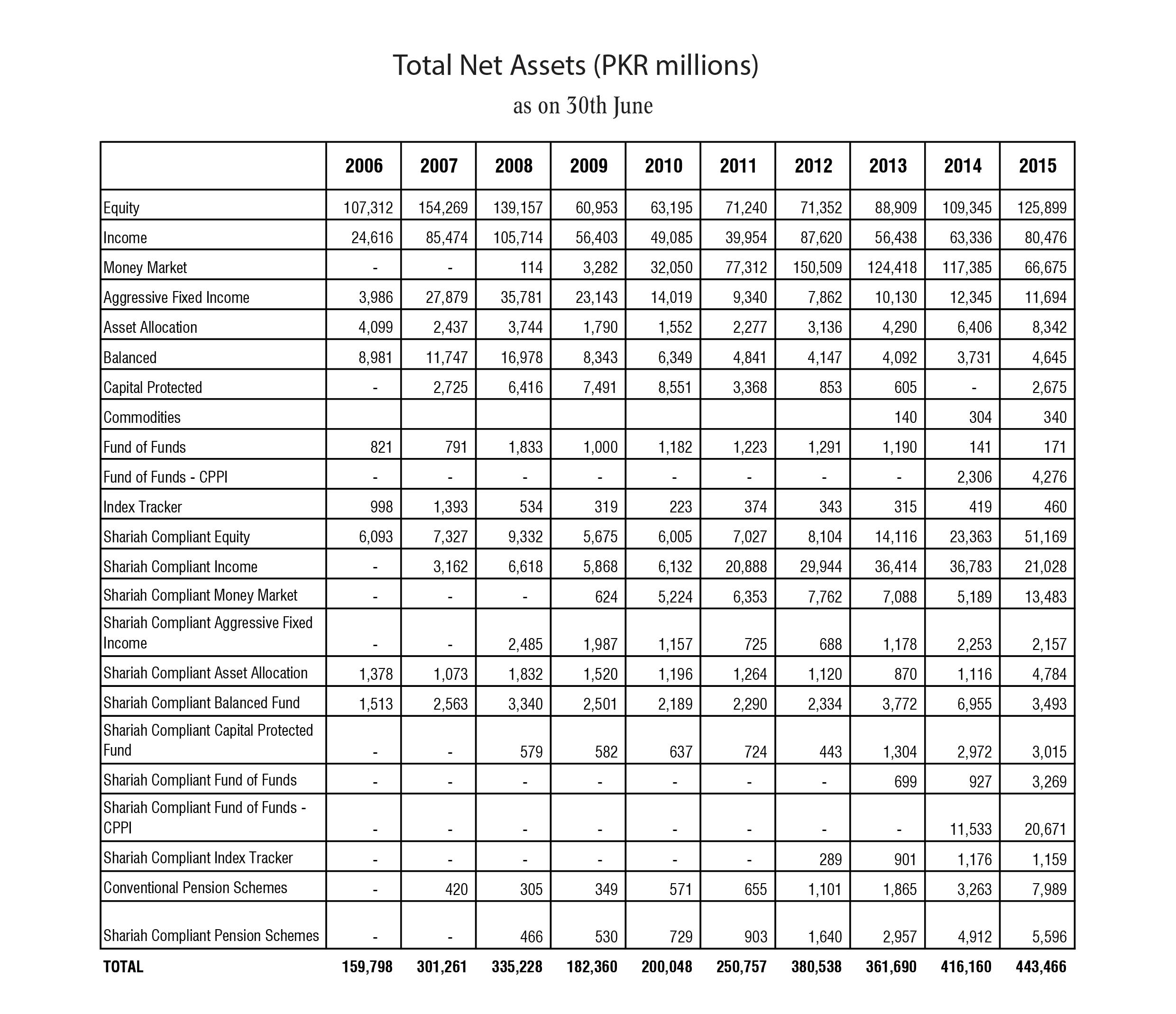

The growth trend in these is as shown in the table below:

Therefore, an investor has a range of mutual funds to chose from for investment and investments should be made in a mix of funds keeping in consideration one's objectives of savings/investments which includes: Return needs, Risk Tolerance, Time horizon and Liquidity needs.

Way Forward

- Early resolution of Court cases and removal of tax anomalies

It is important for the mutual fund industry's survival and growth that the tax anomalies are removed and a conducive environment is present for the industry to do its proper role in the economy as it does internationally. Mutual Funds are the biggest savings avenue worldwide which unfortunately has not been the case over here in Pakistan. While on hand Government is offering high returns on fixed rate Government instruments and schemes making it difficult for market return instruments such as mutual funds to compete, on the other hand it is also imposing double taxation and levies on the mutual funds that are not present on other investment avenues.

It is very clear that WWF is not applicable to mutual funds (also supported by the relevant Ministry of Labour) and yet the matter has been pending since June 2010. Similarly, double taxation on savings products like FED and the sales tax jurisdiction conflicts between SRB & PRA has only resulted in resources to be diverted to fight these in courts instead of being employed to expand and grow the savings rate in the country. A level playing field between mutual funds and other savings and investment avenues is must for mutual funds and pension funds industry to grow and promote savings and investments in the country which is currently at the lowest in the region. MUFAP understands the significance of the issue for investor and industry interest and is actively following up its resolution through the Courts and Government of Pakistan.

- Public Awareness and Education to Expand the Retail Investor Base

It is imperative for long term sustainable growth of the mutual funds industry that the retail investor base increases. Asset Management Industry vis-a-vis the Banking Sector presents a bleak picture, not only in terms of assets under management, but also with regard to participation and outreach to the general public. Currently, asset management companies are offering a diversified range of mutual and pension funds to meet the risk appetite of investors, yet the awareness in the masses is lacking of the options available to them. The industry's next focus must be on conducting a comprehensive and sustained public awareness campaigns to bring across to the attention of the individual investors, the diverse investment features and benefits that mutual funds and voluntary pension schemes offer to them. The Government and SECP are also required to facilitate asset managers to promote, educate and encourage investors to save.